All Categories

Featured

Table of Contents

At the end of the day you are purchasing an insurance item. We enjoy the security that insurance coverage provides, which can be gotten much less expensively from a low-cost term life insurance coverage plan. Unsettled financings from the policy may likewise minimize your fatality advantage, reducing an additional level of defense in the plan.

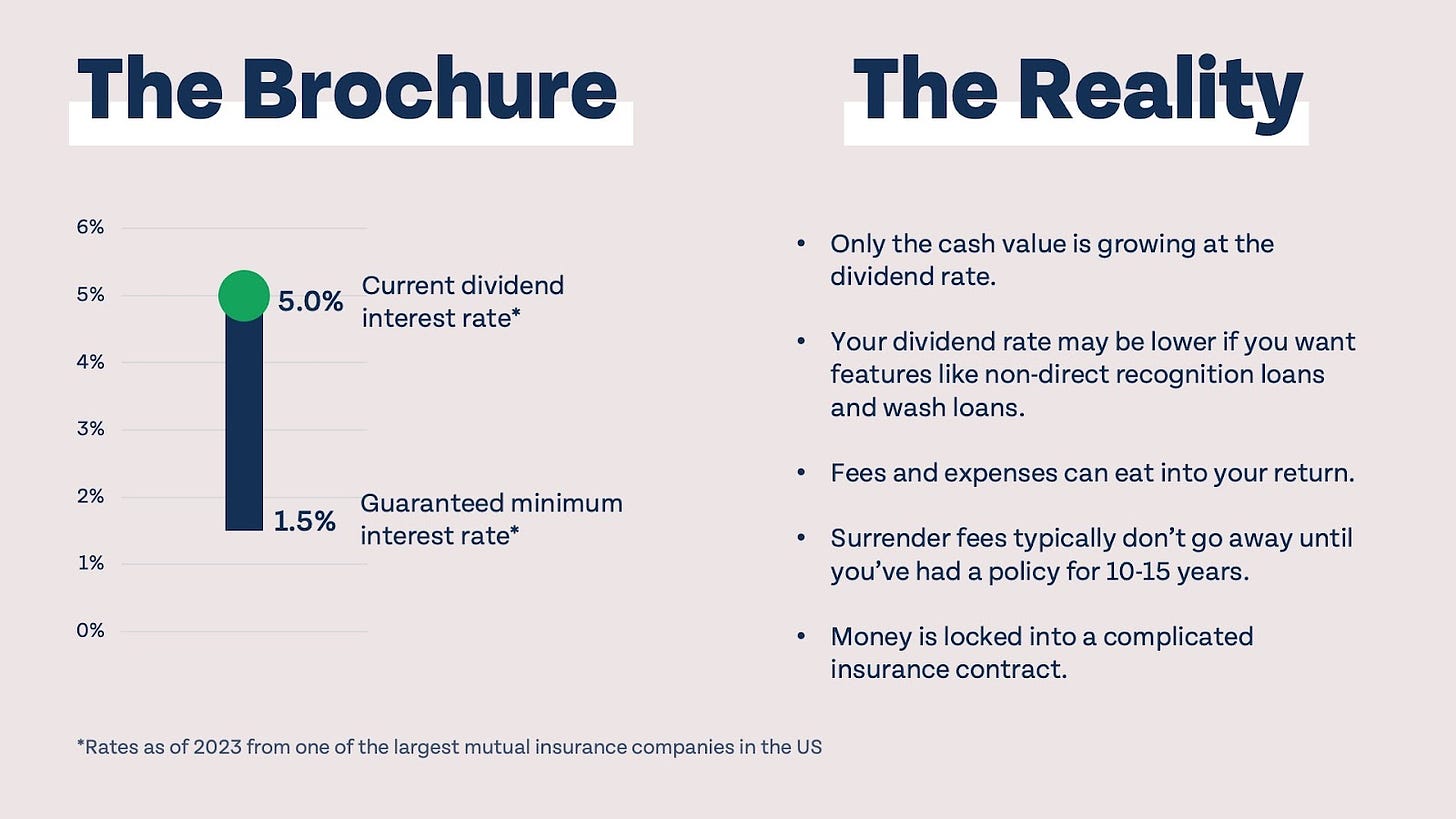

The principle just functions when you not only pay the substantial premiums, yet make use of added cash money to purchase paid-up additions. The possibility price of all of those dollars is remarkable very so when you might rather be purchasing a Roth IRA, HSA, or 401(k). Even when contrasted to a taxed investment account or perhaps a financial savings account, boundless banking might not offer comparable returns (compared to investing) and equivalent liquidity, accessibility, and low/no cost structure (contrasted to a high-yield savings account).

When it comes to economic preparation, entire life insurance frequently stands out as a preferred choice. While the concept may seem attractive, it's crucial to dig much deeper to comprehend what this truly implies and why checking out whole life insurance coverage in this way can be misleading.

The idea of "being your own financial institution" is appealing because it recommends a high level of control over your funds. This control can be imaginary. Insurance provider have the supreme say in exactly how your policy is taken care of, consisting of the terms of the finances and the prices of return on your cash money value.

If you're taking into consideration entire life insurance, it's important to view it in a broader context. Whole life insurance policy can be an important device for estate planning, giving an assured death benefit to your beneficiaries and possibly providing tax obligation advantages. It can likewise be a forced financial savings automobile for those that have a hard time to save cash regularly.

It's a kind of insurance policy with a cost savings part. While it can provide constant, low-risk development of cash worth, the returns are normally lower than what you may accomplish through other financial investment lorries (paradigm life infinite banking). Before delving into whole life insurance coverage with the concept of limitless banking in mind, make the effort to consider your economic goals, risk resistance, and the full variety of financial items offered to you

Infinite Bank Statement

Limitless financial is not an economic panacea. While it can operate in particular situations, it's not without risks, and it calls for a substantial commitment and recognizing to take care of successfully. By recognizing the possible mistakes and recognizing real nature of whole life insurance policy, you'll be much better outfitted to make an informed decision that supports your economic well-being.

This book will certainly educate you just how to establish up a financial policy and how to make use of the banking policy to buy realty.

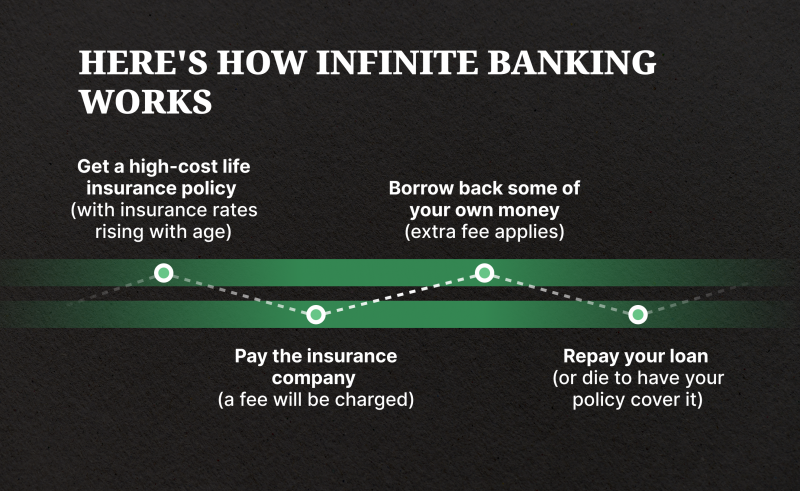

Boundless financial is not a services or product provided by a particular organization. Limitless financial is a strategy in which you acquire a life insurance policy policy that collects interest-earning cash worth and secure loans versus it, "borrowing from on your own" as a resource of resources. After that ultimately repay the funding and start the cycle all over once more.

Pay policy premiums, a section of which develops cash value. Take a loan out against the plan's money worth, tax-free. If you use this concept as planned, you're taking money out of your life insurance coverage policy to acquire everything you would certainly need for the rest of your life.

The are whole life insurance and global life insurance. The cash value is not included to the death benefit.

After ten years, the cash money worth has actually grown to roughly $150,000. He secures a tax-free funding of $50,000 to begin a service with his sibling. The plan lending rates of interest is 6%. He pays off the loan over the next 5 years. Going this path, the rate of interest he pays returns into his policy's money value rather of a financial organization.

The Infinite Banking Concept

Nash was a finance expert and fan of the Austrian institution of business economics, which supports that the worth of items aren't clearly the result of conventional financial structures like supply and demand. Rather, people value cash and goods differently based on their financial condition and demands.

One of the challenges of typical financial, according to Nash, was high-interest prices on financings. Too lots of individuals, himself consisted of, got involved in financial difficulty because of dependence on financial organizations. Long as financial institutions established the interest prices and car loan terms, individuals didn't have control over their very own riches. Becoming your very own banker, Nash determined, would put you in control over your monetary future.

Infinite Financial requires you to have your financial future. For ambitious individuals, it can be the very best monetary tool ever before. Below are the benefits of Infinite Banking: Perhaps the solitary most valuable element of Infinite Financial is that it boosts your cash money circulation. You don't require to experience the hoops of a typical bank to obtain a financing; just request a policy financing from your life insurance policy business and funds will be made readily available to you.

Dividend-paying entire life insurance policy is very reduced risk and offers you, the policyholder, a terrific offer of control. The control that Infinite Financial offers can best be grouped right into two categories: tax advantages and property defenses. Among the reasons whole life insurance is excellent for Infinite Banking is just how it's exhausted.

When you use entire life insurance policy for Infinite Banking, you participate in a personal contract between you and your insurance provider. This personal privacy supplies certain possession securities not located in various other financial cars. These protections might differ from state to state, they can consist of security from possession searches and seizures, defense from judgements and defense from lenders.

Entire life insurance policy plans are non-correlated possessions. This is why they function so well as the economic structure of Infinite Banking. No matter what occurs on the market (stock, property, or otherwise), your insurance coverage retains its well worth. A lot of people are missing this essential volatility barrier that aids secure and grow wide range, instead splitting their cash right into two pails: checking account and investments.

Rbc Royal Bank Visa Infinite Avion

Market-based financial investments grow wealth much quicker yet are subjected to market fluctuations, making them naturally dangerous. Suppose there were a 3rd bucket that supplied security but also modest, surefire returns? Entire life insurance policy is that third bucket. Not only is the rate of return on your whole life insurance policy plan assured, your survivor benefit and premiums are likewise assured.

Here are its main advantages: Liquidity and accessibility: Plan fundings offer immediate access to funds without the constraints of typical bank fundings. Tax obligation efficiency: The money value expands tax-deferred, and policy financings are tax-free, making it a tax-efficient device for developing riches.

Asset protection: In numerous states, the cash money worth of life insurance policy is safeguarded from financial institutions, including an additional layer of monetary safety and security. While Infinite Banking has its merits, it isn't a one-size-fits-all option, and it features significant drawbacks. Right here's why it may not be the most effective approach: Infinite Financial typically calls for complex plan structuring, which can confuse policyholders.

Imagine never ever having to fret about small business loan or high rates of interest once again. What if you could borrow cash on your terms and build wide range all at once? That's the power of boundless banking life insurance policy. By leveraging the cash value of entire life insurance IUL plans, you can grow your riches and obtain money without depending on conventional financial institutions.

There's no collection funding term, and you have the freedom to choose the repayment routine, which can be as leisurely as paying off the financing at the time of death. This adaptability expands to the servicing of the lendings, where you can choose for interest-only repayments, keeping the lending equilibrium level and workable.

Holding money in an IUL dealt with account being credited interest can commonly be much better than holding the cash on deposit at a bank.: You've constantly desired for opening your own pastry shop. You can borrow from your IUL plan to cover the initial expenditures of renting out an area, buying tools, and hiring team.

Infinite Banking Course

Individual loans can be gotten from typical financial institutions and credit unions. Obtaining money on a credit score card is generally really expensive with yearly percent rates of passion (APR) usually getting to 20% to 30% or more a year.

The tax therapy of plan loans can differ considerably depending on your country of house and the specific regards to your IUL plan. In some regions, such as The United States and Canada, the United Arab Emirates, and Saudi Arabia, plan finances are usually tax-free, providing a significant benefit. Nonetheless, in various other territories, there may be tax obligation implications to consider, such as potential tax obligations on the loan.

Term life insurance only provides a death advantage, without any type of money worth accumulation. This suggests there's no cash money value to borrow against.

For car loan policemans, the extensive guidelines enforced by the CFPB can be seen as troublesome and limiting. Funding officers frequently say that the CFPB's policies produce unneeded red tape, leading to more documents and slower finance handling. Regulations like the TILA-RESPA Integrated Disclosure (TRID) regulation and the Ability-to-Repay (ATR) needs, while targeted at shielding consumers, can cause delays in shutting deals and enhanced functional costs.

{kind=link}

Latest Posts

Be Your Own Bank With Life Insurance

Infinity Banking

Banker Life Quotes